Part 2: Advisors and advisory shares: 83(b) election, 409A valuation, vesting, termination and technical/legal side of things

As pre-seed investors, we often provide guidance to the founders of our companies on questions related to equity compensation for advisors. In this series of articles, we aim to provide a comprehensive guide to these topics. As a founder or advisor, you can use this guide as a reference while discussing equity compensation terms, and we are happy to provide additional assistance if you have further questions.

This is the second part of our guide. It covers questions about vesting, termination, 409A valuation, restricted stock awards (RSA), non-qualified stock options (NSO), and 83(b) election. Check out Part 1 here. Should you have any further questions, let’s talk. You can get in touch or follow me on LinkedIn.

What is the vesting for advisors?

There can be two major triggers of vesting: (1) time & (2) milestones. You pick time-based vesting if the value of advising comes from the ongoing interactions and it’s hard to define a specific set of outcomes attributable particularly to the advising. You pick milestone-based vesting if there is a very clearly defined goal for advising and the achievement can trigger the vesting.

When it comes to time-based vesting, the following matters:

- prior experience/relationship. If you have extensive prior experience with the person and they’ve constantly delivered, then you might even skip the vesting schedule.

- timing/long-term duration/continuity of advice. For instance, long vesting makes little sense with an intense short-term support period with an expectation of an immediate effect.

2 years seems to be the most common vesting period for advisors. In theory, you can set a longer vesting period, but in practice, you will most likely outgrow the advisor as you move to your next stage and you will hardly need them with the same intensity after 2 years.

Advisory shares are typically free of a cliff period. Cliff is the period by the end of which you can terminate the contract without giving up any shares to the advisor. The absence of the cliff period in your arrangement assumes you know the advisor sufficiently well or you expect to receive value from them right away (e.g. because the advisor started giving you value even before any advisory arrangements).

Overall, the cliff and vesting period reflect the expected involvement of the advisor. The closer it is to reality, the better it is for everyone.

Avoid people who impose advisory arrangements on you right away, before any practical proof of their value.

What if I want to terminate advisory agreements before vesting ends or before even the cliff period?

Before answering that exact question, here is an idea that may sound controversial to advisors and awkward to implement for founders. Go for fewer shares with a vesting period that reflects the real value exchange. It’s better than getting more shares with longer vesting and the risk of becoming irrelevant to the company after a while.

There may be many reasons why advisory agreements should be terminated, such as conflicts of interest (working for a competitor, starting a competitive company), or mismatch of mutual expectations.

Whatever the reason, if you had a thorough discussion with your advisor before onboarding them, then most probably the situation can be handled much easier. Here are the key things to consider:

- if you are an advisor and the founder asked you to terminate the agreement, you should terminate, unless you know very clearly why you shouldn’t. This is a matter of your reputation and long-term relationship;

- if you are a founder, and you want to terminate the agreement, be prepared to have well-grounded reasoning. The ideal outcome is that you remain friends after it, but you can’t keep everyone happy; and

- whatever you do, make sure you have a lawyer to review your documents and if there are disagreements address them in a separation and release agreement ensuring that the company gets to keep the relevant IP that may have been generated by the Advisor throughout the advisory relationship.

What happens if the company is acquired before the advisory shares are vested?

It’s simple, all shares vest upon the transaction (i.e., any vesting that remains on the advisor's equity award is typically accelerated in full (single trigger acceleration) so that the advisor can reap the full benefit of their advisory services). However, sometimes the stock award agreement may provide for an additional event to fully vest the shares (double trigger acceleration). Those are not common for advisors, but can be part of the contractual arrangement due to using wrong templates or poorly negotiated terms.

The technical/legal side of things. Non-qualified Stock Options vs Restricted Common Stock for startup advisors.

Now, when you know who, why, how much, and for how long, it’s time to have a look at the legal side of things. There are 2 main ways to issue stock to an advisor under a vesting schedule: (1) NSO or non-qualified stock options, and (2) RSA or restricted stock award. Let’s define each of those and have a look at the pros and cons.

First, let’s establish something: generally, the IRS treats the fair market value of the shares you receive from a startup in exchange for your services as income, and just like any other income you must pay taxes on the value you received. For example, if you receive 10,000 shares of a company with per share value of $1, then the IRS thinks that you received a check for $10,000, therefore, you must pay taxes on this amount.

Non-qualified Stock Options (NSO): NSOs are an option to purchase a company's shares sometime in the future at a pre-set price (also known as strike price or exercise price). An option gives the option holder the right (but not the obligation) to “exercise” the option and buy the shares. The act of claiming the right and purchasing shares at the pre-set price is called “exercising” the option.

Unlike Incentive Stock Options (ISO), a company may issue NSOs to all types of service providers (e.g., advisors, consultants, directors, independent contractors, etc.), and does not have to issue those at fair market value, as well as does not have to comply with all of the documentary requirements and holding period restrictions applicable to ISOs.

NSOs, however, do not qualify for the favorable tax treatment afforded to ISOs. Instead, NSOs are generally taxed upon exercise at ordinary income tax rates, based on the difference between the exercise price and the fair market value of an underlying share on the exercise date (often referred to as the “spread”).

For the purposes of this article, it does not make much sense to discuss the difference between incentive stock options (ISOs) and NSOs because ISOs can be granted only to employees. Just be aware that the main difference is the taxation rate: while gain from ISO exercise is taxed as a capital gain, the gain from NSOs is taxed as ordinary income (ordinary income tax rate is generally higher than preferential tax rates on capital gains that applies to ISOs).

A restricted stock award (RSA) is a grant of a company's common stock in which the recipient's rights in the stock are restricted until the shares vest (or lapse in restrictions). Unlike NSO, where we have the right to purchase in the future, in the case of RSA, it is an actual grant of shares – the company, however, reserves the right to forfeit or repurchase the unvested stock. Shares of restricted stock are actual shares of the company’s common stock that carry restrictions on transfer and sale that lapse (usually, but not necessarily, in installments) over a specified vesting period or upon the achievement of specified vesting conditions.

Vesting means that the advisor has a non-forfeitable right to the stock, meaning that the restrictions are lifted on the vested portion of the RSA.

Companies frequently use restricted stock (like other types of equity grants) as a retention tool by requiring the advisor to continue providing services to the company through each vesting date. Some companies, however, will accelerate the vesting of restricted stock upon a change in control and may even accelerate vesting upon certain types of terminations (for example, terminations without cause, for good reason, or due to death or disability).

Because shares of restricted stock are issued upon grant, the holders of restricted stock generally have the same or similar dividend rights and voting rights as other shareholders.

The choice between the two comes down to tax consideration, so this is what we are going to focus on. Comparing the two, both RSAs and NSOs allow for a deferral of taxable income beyond the grant year. The deferral period for restricted stock depends upon the date it vests (i.e., is no longer subject to vesting or a substantial risk of forfeiture), whereas the deferral period of an NSO can be stretched out by the holder until exercise. As a result, the economic advantage of restricted stock is generally offset by the lack of control over vesting, whereas the economic disadvantage of an NSO is offset by having control over the timing of exercise. This is one reason many people prefer options over other forms of equity-linked compensation with fixed vesting or settlement dates.

409A Valuation

Additionally, let us quickly check out the 409A valuation. A 409A valuation is an independent appraisal of the fair market value (FMV) of a private company’s common stock (the stock reserved for founders, employees, and advisors) conducted by a third-party expert (such as Carta) or the Board of Directors. This valuation determines the cost to purchase a share.

Long story short: you can’t offer equity without knowing how much a share is worth, and you need a 409A valuation to know that. The good news (from a tax perspective) is that a 409A valuation has very little to do with your SAFE valuation cap.

Even though the SAFE valuation cap is a good estimate of the company valuation in the world of venture capital, in the world of taxes, you include many risk factors in the estimates, which significantly (50-90%) reduces the estimate for the so-called fair market value of your common stock. This is because, under Section 409 of the Internal Revenue Code, SAFEs are not listed as a material event (unlike selling equity/stock or notes in the company) that would trigger a periodic determination of the FMV of a startup's shares.

How much are NSO taxes?

There are three main taxation triggers with NSOs:

- Grant / receipt of NSOs. The moment the advisor receives NSO, they should pay an income tax from the difference between the fair market value of the underlying shares and the exercise price (e.g., if you got an NSO to purchase 10,000 shares at an exercise price of $10, while the fair market price per share is $20.00, then you have a $100,000 taxable income ($200,000 - $100,000 = $100,000)[1]. Therefore, it is important to get a 409A valuation to have the reference point for the fair market value.

- Exercise of the NSOs. If and when you exercise the NSOs, you would have ordinary income based on the difference between the exercise price and the then-current fair market value of the shares. For example, if you exercised the NSO to purchase 10,000 shares at an exercise price of $10 per share, and the shares are then worth $50.00 per share, you would have $400,000 of taxable income ($500,000 - $100,000 = $400,000).

- Sale of shares. If and when you sell the shares, you would recognize either a short-term or long-term capital gain (assuming appreciation in value of the shares), depending on whether the shares are held for at least one year, based on whether the sales price is more or less than $10 per share (your new basis in the shares as a result of your having recognized taxable income at the $50 per share valuation).

Knowing the above, it is reasonable to assume that the most logical way of dealing with NSOs at very early stages is receiving those with an exercise price equal to market value (typically a very small amount) and exercising only when there is a liquidity event or the stock is liquid/worthy enough, so you don’t have to pay real taxes for the paper value of the shares. This requires staying in close contact with the founders to be aware of the timing of the exit.

Ideally, you want to exercise the NSO 12 months prior to the exit to qualify for preferential tax rates for capital gains.

Startup option plans usually require that vested options be exercised within 3 months of termination of the advisor agreement or else they expire. This is done to reduce the “uncertainty” on the cap table as each option is a right to purchase shares without certainty whether this right will be utilized. However, at very early stages it seems to be a better idea to skip imposing any deadlines on an advisor.

Given that the exercise price is usually nominal at an early stage, it may make sense to exercise the NSOs right away if those are given without a vesting schedule. This will result in no additional tax event at the point of exercise and usually lower capital gain tax when there is a liquidity event. However, in case there is a vesting schedule in place[HM1], the exercise may become a taxable event because, by the time when vesting ends, the fair market value of the shares may be significantly higher[HM2]. Therefore, advisors should weigh pros and cons before making the final decisions.

How are RSAs taxed and what’s the difference from NSOs?

Restricted stock is generally not taxed upon grant. Instead, the advisor will recognize taxable income if and when the shares no longer face a substantial risk of forfeiture (i.e., on vesting). However, an advisor may elect to recognize taxable income in the year of grant in an amount equal to the fair market value of the shares at the time of grant, by filing an Internal Revenue Code section 83(b) election with the Internal Revenue Service and the company within 30 days of the grant date.

The 83(b) election is simply an informational notice that states the election made by the taxpayer and describes certain terms of the award. If the advisor properly and timely files this 83(b) election, the advisor will immediately recognize income equal to the difference, if any, between the fair market value of the shares upon grant and the price paid for the shares.

Why do this?

Because generally, the fair market value of startup shares you receive is much lower (sometimes nominal - $0.00001) at the early stage rather than after startups raise funding and gain traction. Given the fact that vesting schedules typically range from 1-3 years, you may be better off fixing the fair market value of your stock for tax purposes when the stock is issued to you by filing the Section 83(b) election to minimize your tax burden. For example, you get 10,000 shares on a 3-year vesting schedule with the fair market value of $0,00001. This means that the income recognized will equal only $0.1 if you file the Section 83(b) election.

Imagine, the valuation of the startups reaches millions and per share price is $1 per share by year 4. Therefore, the value of your stock is much higher which triggers much higher tax obligations. Note that, in addition to accelerated income inclusion, the Section 83(b) election causes the holding period for the property to begin at the transfer date, rather than from the vesting date for characterization as a short- or long-term capital gain.

Making a Section 83(b) election advantages the advisor in that the subsequent vesting of the stock will not result in a taxable event, because the advisor has already paid the required tax. Further, if the advisor later sells the vested shares in a taxable transaction, any appreciation in the value of the shares since the grant date will be taxed at capital gains rates, rather than the typically higher rates applicable to ordinary income. This is one of the main benefits of the Section 83(b) election.

On the other hand, if the advisor files a Section 83(b) election on restricted stock that is later forfeited before vesting (due to, for example, a termination of employment before the vesting date), the advisor will not be able to claim a deduction for the amount reported as income at the time of grant, or for excess taxes paid as a result of making the election. Section 83(b) elections, once filed, cannot be revoked.

Because restricted stock is considered “property” subject to the Section 83(b) election, the requirements of Internal Revenue Code section 409A (Section 409A) do not apply.

The taxation of RSAs significantly depends on the Section83(b) election, especially if there is a vesting schedule in place. 83(b) election allows the recipient of stock not to pay taxes when shares vest and only pay whenever the equity is sold. By default, vesting is seen by the IRS as an income the company paid you with the stock, so you must pay taxes (more about 83(b) election is available in Armine Galstyan’s article on filing 83(b) election from Europe).

The Section 83(b) election allows the advisor to pay the taxes due on the acquisition of the unvested stock in the year of exercise (instead of at a later time as the issued shares vest), at ordinary income rates calculated on the difference between the exercise price of the unvested stock and its fair market value (FMV) on the option exercise date. If the advisor exercises the option immediately after grant, in most cases, the FMV will be the same as the exercise price, meaning the advisor pays $0 in taxes on the acquisition of the stock.

Early exercising, however, is not without disadvantages. When the advisor exercises their stock option early and files a Section 83(b) election, the advisor takes the risk that they will lose the money paid for the stock. If the startup fails, the startup’s stock will have no value. Another drawback of early exercise is that, even where the startup’s shares increase in value, the acquired stock may be illiquid for many years.

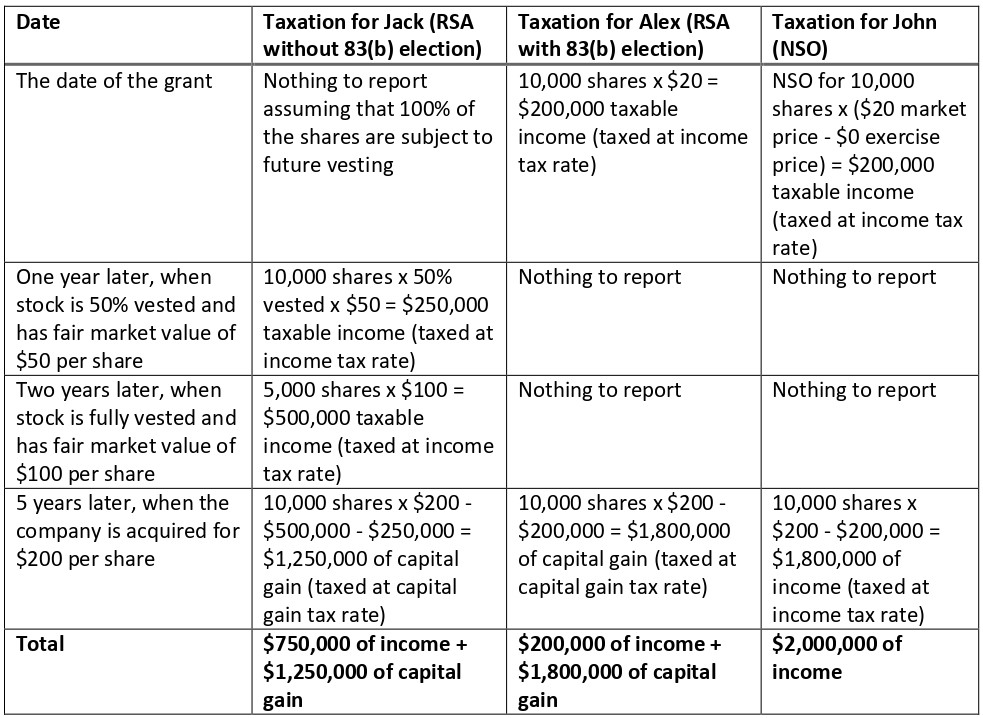

The example below demonstrates the effect of 83(b) election on taxes. Jack, Alex, and John are all advisors. Jack and Alex each receive RSAs of 10,000 shares for zero dollars and 2 years vesting period. John receives NSOs for 10,000 shares with an exercise price of zero dollars per share and the same 2 years of vesting*. The fair market value of the stock is $20 per share on the grant date as per the 409A valuation. Jack decides to declare the stock at vesting while Alex opts for the Section 83(b) election treatment. Here is what happens next:

The difference between the first two is significant:

- Capital gain tax is usually lower than income tax.

- Jack pays taxes with real cash against the paper value of the stock, while Alex pays most of the cash only after cashing out from the company herself. Imagine the startup fails in year 3: Jack will end up with taxes paid for $750K worth of income, while Alex only $200K.

However, there is a substantial risk of forfeiture associated with the Section 83(b) election. If Alex terminates the agreement before the plan becomes vested, all rights to the entire stock balance could be relinquished, leaving Alex without advisory shares and real cash expense for taxes without any refund. This is a major disadvantage of the Section 83(b) election.

As for the NSOs, there apparently can be other scenarios of exercise, but those scenarios will involve more cash expense on taxes prior to the liquidity event.

Another important aspect to consider is that the exercise price is a real price that an advisor is supposed to pay to the company to receive the stock. In our example above, the exercise price for John was zero, however, should it be, say $10 per share, John would be required to pay $100K to the company to become a shareholder. This said, if the option holder exercises the stock option immediately or soon after the grant date, then the exercise price will most likely be very low and lead to little or no taxes upon exercise (assuming the fair market value of the company’s common stock has not changed or has only increased slightly). If you choose to do so, do not forget to file an 83(b) election to avoid taxes upon vesting.

Long story short: NSOs allow for the lowest upfront tax payment, RSAs with 83(b) election allow for lowest overall tax expense with most of the tax being paid upon liquidity event, and NSOs with early exercise and small fair market value at the date of exercise are essentially equivalent of the RSAs if you go with 83(b) election. VERY important note: IRS should receive the 83(b) election within 30 days of acquiring the stocks (issuing the stocks). Once the deadline is missed, there is no way to fix this!

Non-U.S. resident advisors need to check for possible tax implications locally.

All the above taxation considerations are relevant to U.S. tax residents only. If the advisor is not a U.S. tax resident and provides the advisory services while physically being outside the U.S., there are no taxes to be paid in the U.S. Each advisor should check his/her own jurisdiction for possible tax obligations.

Note that people can be liable for taxes both in the country or countries of residence and country or countries of citizenship. For example, if the advisor is a resident of the Republic of Armenia, no tax obligation is accrued in Armenia as long as there is no cash-out event.

The US is a tricky system, even if you’re not in the US:

- US citizens residing anywhere are considered US residents for tax purposes.

- US non-citizen “green card” holders are likewise usually considered US residents for tax purposes (and will lose their green card if they don’t file taxes).

- If you drop US citizenship, there is an exit tax.

Luckily the U.S. system is also the best understood system for startups.

Is there a standard package of documents for advisory shares?

As a founder, you probably look for a standard package of documents that would make the issuing of advisory shares as easy as it is in the case of fundraising with SAFE. The short answer is that there is no such comprehensive solution; however, some tips may be helpful.

There are two sets of documents that regulate the advisory share grant: (1) advisory services agreement and (2) issuance of RSAs or NSOs from a plan. Technically, you can sign the advisory agreement without the actual issuance of the shares or option and simply promise to do so in your advisory agreement.

That makes life very easy for everyone but may have tax implications on the advisor.

For example, if you set up a stock options plan sometime after signing the advisory agreement, and the fair market value of the company increases (typically because you raise a new round), then the advisor will have to pay taxes from the higher stock price on the date of stock issuance. Also, from a legal point of view, executives sign the advisory agreements, but the stock is issued by the Board. So until the stock is issued by the Board there is no transfer of property, hence technically advisors run the risk of not getting their stock if the relationship with the founders deteriorates and the advisory agreement is terminated.

Some founders consider selling stock to advisors at the nominal price in the early days of the company. However, after the initial purchase of stock by the founders, it generally becomes increasingly dangerous from a tax perspective to sell stock at the same price per share to advisors. The issue is that tax authorities may claim that the purchase price of the stock was lower than the fair value, and thus, the difference between the two should be reported as taxable compensation.

Typically, a company can sell common stock to advisors only very early on, cease any issuances at all for a while, then adopt a stock plan and get a 409A valuation to set the price of issuances from the plan.

It is generally not recommended for companies to set up stock plans and use them on their own without the assistance of a lawyer. Issues related to taxes, incorrect authorization of shares, or other issues may become a headache.

The most reliable method is to set up a stock plan on Clerky with a lawyer as a reviewer, and then delay stock issuances as long as possible, ideally until the company has the money to pay for the lawyer(s) to help them with the issuances (e.g., in connection with a Series Seed or Series A). Many startups use Carta for their cap table management.

* A company can set exercise price below the prevailing market price or at any such discounted price but it cannot be below the face value of the shares. We assume the face value is 0 for simplicity of calculations.

Thank you

Huge thank you goes to Hayk Mamajanyan, Partner at Rimon PC, Adam Bittlingmayer, Co-founder and CEO at ModelFront, for comments and suggestions for this article, as well as to Andrew Coleman for editing and proofreading.

Disclaimer

The information provided in this article does not, and is not intended to, constitute legal advice; instead, all information, content, and materials available on this site are for general informational purposes only.

Should you have any further questions, let’s talk. You can get in touch or follow me on LinkedIn.